Article | January 2026

Allianz Risk Barometer 2026 -

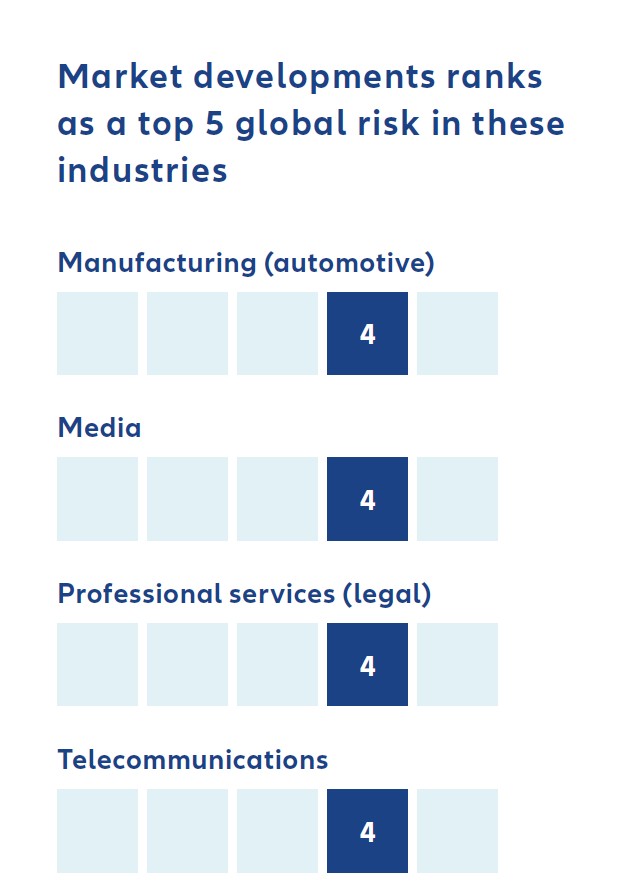

Global risk #10: Market developments (13%)

Following another strong year for equity and M&A markets, businesses appear slightly more relaxed about market risks, with this risk dropping from #8 to #10 year-on-year. Yet how does this square with widespread discussion of an emerging AI bubble?

This article is part of the overview of the most important business risks in 2026, according to the Allianz Risk Barometer 2026.

Perhaps the key lies in the character of the current artificial intelligence (AI) rally: it is arguably one of the least celebrated in recent memory. Unlike the exuberance of the late-1990s dotcom boom, today’s market shows little sign of unbridled euphoria.

Market participants remain cautious. Equity valuations – especially in the US – are undeniably high, although not yet as extreme as during the dotcom bubble. There is still room for valuations to rise before reverting to more normal levels. Crucially, the AI narrative grows more compelling by the day. Evidence of successful adoption is accumulating rapidly, reinforcing expectations that AI will reshape entire industries and lift productivity growth. As a result, AI is expected to remain a dominant market driver in 2026, with the AI cycle likely to hold steady and US technology firms leading the charge. Earnings growth should support solid returns, with equity markets in the US and Europe forecast to deliver year-on-year gains of roughly 11% and 9%, respectively. However, elevated expectations also heighten vulnerability. With technology earnings surging and investors pricing in continued momentum, any signs of slowing – such as missed earnings targets – could quickly undermine confidence. A sharp market correction cannot be ruled out.

Turning to interest rates, long-term yields in 2026 are expected to stabilize around 4.25% for 10-year US Treasuries and 2.5% for German Bunds. In bond markets, fiscal uncertainty remains the chief concern.

Major economies, including the US, are grappling with unsustainable public finances and persistently high deficits at a time when elevated interest rates have pushed up debt-servicing costs. Political shocks could therefore exacerbate fiscal worries and drive yields higher.

In summary: Businesses may be justified in anticipating another resilient year in capital markets marked by robust returns, strong M&A activity and relative rate stability. But there is little room for complacency.

Photo: Shutterstock

Source: Allianz Commercial

Overview

Market developments (e.g., intensified competition / new entrants, M&A, market stagnation, market fluctuation)

Ranking history:

- 2026: rank 10

- 2025: rank 8

- 2024: rank 9

- 2023: rank 11

- 2022: rank 8

- 2021: rank 4

All the latest news, reports and hot topics

Sign up to the newsletter

Keep up to date on all news and insights from Allianz Commercial